PayNow Gen2: Singapore's Infrastructure Bet on the Age of AI Agents

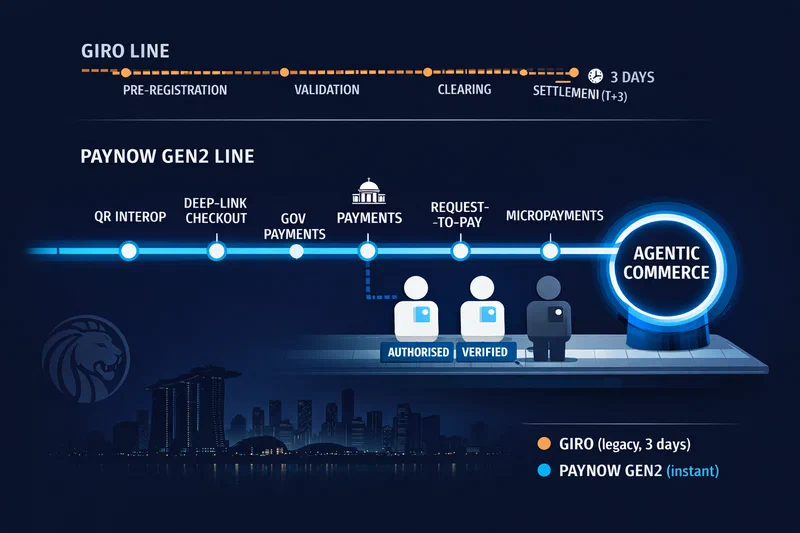

GIRO, Singapore’s legacy interbank payment system, requires pre-registration and takes up to three business days to clear. That timeline made perfect sense when every payment was initiated by a human with a calendar and a bank login.

AI agents have neither.

When a treasury AI instructs a supplier payment at 3 a.m. on a Friday, or an autonomous procurement agent locks in component prices before any human has reached their desk, a three-day settlement window is not an inconvenience — it is a structural incompatibility. This week, Singapore published the blueprint for how it intends to fix that, not just for today’s transactions, but for a payments future where machines may be initiating as many transactions as people.

The PayNow Generation 2: Defining the Next Wave of Innovation for Singapore’s Instant Payments System report, released by MAS and the Association of Banks in Singapore on 25 June, has attracted predictable commentary: QR interoperability, faster government payments, better online checkout. All true. All incomplete.

The more significant story is buried in the long-term capabilities section, in two words that no other central bank’s instant payment roadmap has placed there: agentic commerce.

The agentic commerce context the report is responding to #

Before reading PayNow Gen2 as a payments document, you need to read the market it is responding to.

By Black Friday 2025, AI-driven traffic to US retail sites had risen 805% year-over-year. AI agents drove over $22 billion in global online sales in a single shopping window. The global AI agents market, valued at $5.4 billion in 2024, is projected to reach $236 billion by 2034. Agents are not “coming” to commerce. They have arrived. And they are spending.

The problem is that they are transacting inside infrastructure built for humans. When an AI agent executes a purchase, the verification, authorisation, and settlement machinery underneath that transaction was designed with a human counterpart in mind — someone who could respond to a second-factor prompt, tolerate a GIRO delay, or call their bank when something went wrong. Agents do neither. They escalate to fallback logic or they fail silently.

In February 2026, NIST launched its AI Agent Standards Initiative specifically because this infrastructure gap is creating a fragmented, untrusted agent ecosystem. The IMF published a note in April calling for “Know Your Agent” frameworks — the payments-era equivalent of KYC — with mandated verifiable identities for financial bots linked to legal entities, and cryptographic mandate frameworks that bind agent-initiated transactions to defined scope and limits. Global regulators are diagnosing a problem. Singapore appears to be building the solution.

What the Gen2 report actually says — and what it implies #

The near-term priorities in the PayNow Gen2 report are practical and sequenced, with MAS and ABS having consulted 37 organisations and benchmarked against 11 jurisdictions.

Piloting QR payment interoperability between PayNow and NETS QR by end of 2026 will eliminate friction where customers cannot scan merchant QR codes across schemes. Deep-linking within PayNow QR codes for online checkout — reducing the number of steps before payment confirmation — follows within a year. Larger-value transactions to government agencies, which currently move through the three-day GIRO process, will enter a sandboxed pilot with transaction limits and safeguards.

These are meaningful improvements, each with a clear product rationale. But the long-term capabilities section is where the architectural intent becomes visible.

The report lists request-to-pay, structured data fields for automated reconciliation, micropayments, expanded cross-border connectivity, offline payment capabilities, and — alongside all of these — agentic commerce. Not as a vague aspiration. As a named, designed-for capability in Singapore’s national instant payment infrastructure, with MAS and ABS committing to begin foundational work this year.

That is a first. No other central bank’s instant payment roadmap I am aware of has named agentic commerce as an architectural design target. India’s UPI has been retrofitted for AI agent payments through private-sector additions such as Pine Labs’ recent integration. The UK’s Faster Payments is advancing its overlay services. Brazil’s PIX continues to expand. But none of them have released a national report stating, explicitly: we are building the underlying rails for AI agents to transact here, with designed-in governance, and we will develop the toolkits for it.

The governance layer, announced the same week #

The day after the PayNow Gen2 report, MAS announced the Future of Finance Institute — a coordinating body to help financial firms move AI and tokenisation from pilots to mainstream deployment. The institute will maintain a knowledge hub of validated use cases, provide sandboxes for programmable money and tokenised assets, and develop specific toolkits for agentic AI and programmable compliance. MAS retains the regulatory framework; the institute handles implementation coordination across institutions of all sizes.

These two announcements in the same week are not coincidental. They are the infrastructure layer and the governance layer of the same strategy, released in parallel. Singapore has learned from previous financial technology cycles — digital bank licensing, real-time payments infrastructure, open banking — that neither layer survives without the other. Payment rails without compliance toolkits invite regulatory paralysis. Compliance frameworks without implementable infrastructure remain paper exercises.

The Future of Finance Institute builds on existing MAS-led programmes: the MindForge AI Risk Management Toolkit, PathFin.ai, Project Guardian (tokenisation of real-world assets), and Project Orchid (programmable money). Singapore is not starting from scratch — it is connecting an existing ecosystem of well-governed pilots into a production-scale architecture.

The signal the private sector is sending #

Private sector behaviour in the same week confirms the directional bet.

On 23 June, Backbase acquired Kasisto, a New York-based developer of agentic AI software for banks whose clients include JP Morgan, Standard Chartered, TD Bank, and Westpac. Kasisto’s KAIgentic platform — and its banking-tuned KaiGPT language model — routes AI agent interactions through compliance controls, eligibility checks, policy enforcement, and audit logging before any action executes. Backbase, which reported over $350 million in revenue in 2025 and runs on more than 120 banks globally, bought Kasisto specifically because it needed to embed that compliance architecture into its AI-native Banking OS.

The acquisition tells you what the banks that have actually engaged with agentic banking as a product problem have concluded: the entity presenting a payment instruction may now be an AI acting on behalf of an account holder, and the underlying rails need to be built for that entity. Not retrofitted for it. Built for it.

Singapore is building those rails nationally. Backbase is building them commercially. The convergence is not accidental.

The shadow that follows the blueprint #

There is a risk that deserves proportionate attention, and the PayNow Gen2 report does not dwell on it.

Agentic infrastructure is also fraud infrastructure.

A BioCatch survey published this week, covering 1,440 fraud management and financial crime professionals across 25 countries, found that 80% of financial institutions have already experienced an attack carried out by an AI agent. Boston Consulting Group estimates that agentic AI slashes the cost of executing financial fraud schemes by over 90%, and forecasts that autonomous agents could more than double successful fraudulent activity. In the Asia-Pacific region, 79% of surveyed institutions reported encountering agentic AI attacks. The Interpol 2026 Global Financial Fraud Threat Assessment, released in March, separately warns of escalating deployment of AI agents in criminal operations — systems that can autonomously plan entire fraud schemes, test tactics at scale, and adapt against new defences in real time.

The same programmable payment rails that will let a corporate treasury AI settle a supplier invoice at 3 a.m. will be probed, tested, and potentially exploited by autonomous fraud agents operating at the same speed and at far greater scale. Singapore’s MindForge toolkit and the Future of Finance Institute’s planned agentic AI and programmable compliance toolkits are the intended defences. Whether they will be sufficient depends entirely on how quickly the defensive architecture matures relative to the offensive one.

That is the open question sitting beneath the optimism of the Gen2 report, and it is worth holding in mind as implementation begins.

What this means for product and strategy leaders #

If you are building financial products in Singapore, or for Singapore-connected markets across Southeast Asia, the PayNow Gen2 report is not background reading. It is a product architecture signal.

Request-to-pay functionality, once live, changes how collections work and how subscription and recurring payment products are designed. Deep-linking in QR codes will measurably reduce checkout abandonment on mobile — the product implication is a redesign of how e-commerce conversion funnels are instrumented. Structured data fields for automated reconciliation will finally let operations teams retire the spreadsheet bridges between instant payments and accounting systems.

More broadly: for anyone building agentic AI products that touch payments, in any sector, Singapore has just told you where the interoperable, governance-anchored, programmable payment future is being built first. The question worth asking today, not in 2027, is whether your product architecture is positioned to participate in it.

The rest of the world is still writing committee papers. Singapore has already poured the concrete.

References

- Fintech News Singapore (June 26, 2026). “PayNow Could Move Beyond Transfers as Singapore Studies Gen2 Upgrades.” https://fintechnews.sg/133667/payments/paynow-gen2/ (Accessed June 30, 2026)

- Fintech News Singapore (June 26, 2026). “MAS Sets Up Future of Finance Institute to Move AI, Tokenisation Beyond Pilots.” https://fintechnews.sg/133708/ai/mas-future-of-finance-institute/ (Accessed June 30, 2026)

- Fintech News Singapore (June 23, 2026). “Backbase Acquires Kasisto, Deepening its Push into Agentic Banking.” https://fintechnews.sg/133517/ai/backbase-aqcuires-kasisto-agentic-banking/ (Accessed June 30, 2026)

- PYMNTS (June 29, 2026). “Why It’s Time to Know Your Agent.” https://www.pymnts.com/news/artificial-intelligence/2026/why-its-time-to-know-your-agent/ (Accessed June 30, 2026)

- Fintech News Singapore (June 29, 2026). “The Rise of Agentic AI in Cyber Fraud and Scams.” https://fintechnews.sg/133560/ai/the-rise-of-agentic-ai-in-cyber-fraud-and-scams/ (Accessed June 30, 2026)

AI-Generated Content Notice

This article was created using artificial intelligence technology. While we strive for accuracy and provide valuable insights, readers should independently verify information and use their own judgment when making business decisions. The content may not reflect real-time market conditions or personal circumstances.

Whenever possible, we include references and sources to support the information presented. Readers are encouraged to consult these sources for further information.

Related Articles

SEA Weekly: After Liberation Day — What Southeast Asia Built Instead

The tariff anniversary week that mattered wasn’t for what it revealed about factories. It was …

SEA Weekly: Consolidation and Control — Southeast Asia's Digital Finance Enters a New Phase

This week: Kredivo buys its way into Vietnam via the Timo acquisition, an IMF report confirms …

The Token Capital Trap: Why Enterprise AI Costs Are Inverting the Economics of Software

Uber blew its annual AI budget in four months. Microsoft cancelled Claude Code licenses mid-year. …